The Lloyd's distribution problem hidden inside the Zurich-Beazley deal

The Lloyd's distribution problem hidden inside the Zurich-Beazley deal

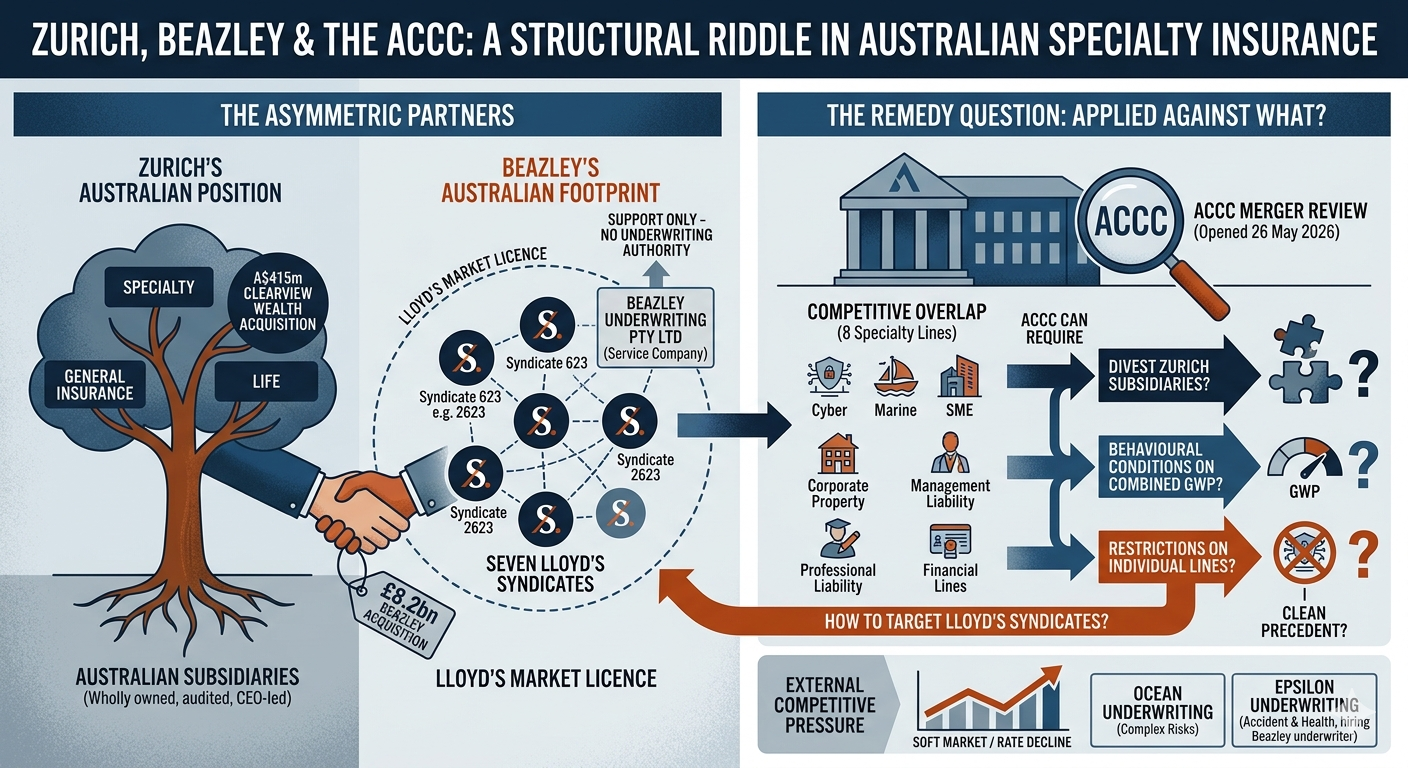

The ACCC opened its formal review of Zurich's £8.2bn Beazley acquisition on 26 May 2026, listing competitive overlap across eight specialty lines: cyber, marine, SME, corporate property, personal accident, management liability, professional liability, and financial lines. Initial assessment runs to 7 July. Public feedback closes 2 June.

That list is the entire specialty product set Beazley writes into the Australian market. Which is a problem with a particular shape, because Beazley does not write in Australia through a domestic subsidiary. It writes solely through the seven Lloyd's syndicates it manages.

This is the structural question the ACCC review surfaces. When competitive remedies have to be applied to a carrier whose entire Australian distribution sits inside Lloyd's, what does remediation actually look like? The market does not have a clean precedent.

A structural asymmetry

Zurich's Australian position is the opposite of Beazley's. The Swiss insurer operates through wholly owned subsidiaries offering general insurance, specialty, and life cover. It is concurrently acquiring ClearView Wealth in Australia for A$415m, with completion targeted for Q3 2026. Zurich Australia and NZ has a named CEO, audited Australian books, and a regulator-facing operating structure.

Beazley's footprint sits inside the Lloyd's market structure. Sydney office opened in 2008, with Brisbane added later and around 40 staff between the two. The presence is real, but the distribution layer is Lloyd's. Beazley historically focused on accident, health and contingency lines locally, with the ACCC's list confirming the broader specialty book also reaches Australian buyers through the syndicates.

That asymmetry is what makes the remedy question structurally novel. The ACCC can require Zurich to divest specific Australian subsidiaries, accept behavioural conditions on combined GWP, or impose restrictions on individual lines. Applying any of those against Lloyd's syndicate distribution requires either a remedy targeted at Beazley's specific syndicates, which raises questions about Lloyd's broader market participation, or remedies that target Zurich's domestic business alone while letting the syndicate-routed Beazley book continue unchanged. Neither is a comfortable answer.

How Beazley reaches the Australian market

The distribution mechanics matter for the remedy question. Beazley Underwriting Pty Ltd, the Australian service company, supports the placement of business written by the syndicates rather than holding underwriting authority in its own right. Australian brokers place risks with Beazley through the service company structure, with the actual underwriting capacity sitting on the syndicate balance sheets at Lloyd's.

This is how most Lloyd's specialty carriers operate in Australia. The Lloyd's market itself is Australia's fourth-largest insurance market with a 150-year continuous presence. Capacity reaches Australian buyers through approved coverholders, service companies, and direct placement, all sitting under the Lloyd's licence rather than under individual carrier licences in the domestic market.

The Australian service company supports business in market but does not hold underwriting authority. Underwriting authority sits on the syndicate balance sheets at Lloyd's. The Lloyd's market licence sits over all of it. A remedy structured against any of these layers raises different questions, and none has obvious precedent for the regulatory question now in front of the ACCC.

Competitive pressure outside the regulatory process

The competitive challenge to Beazley's Australian position is also arriving from outside the ACCC process. In February, Ocean Underwriting launched a complex risks liability facility for Australian brokers. In May, Epsilon Underwriting Agency announced a new accident and health division, hiring former Beazley senior underwriter Tim Curling to run it. The division targets medium-to-large group personal accident, sickness, and journey accident covers across construction, mining, and energy. That is the segment Beazley has historically dominated in the local market.

The Australian commercial insurance market remained soft through H1 2026, with rates declining across D&O, professional indemnity, cyber and management liability. Local capacity has continued to expand, with new MGA entrants arriving in directly competitive lines.

The competitive picture has shifted. Senior personnel have departed during the announced acquisition window. Domestic MGA entrants are arriving in directly competitive lines. The pricing cycle is soft. None of these signals required the ACCC's intervention to emerge. The regulatory review is the moment they all become visible together.

A market with deeper history than the moment suggests

The senior personnel pattern is not new. Andrew Horton ran Beazley as CEO from 2008 to 2021 before moving to QBE as Group CEO, an Australian-headquartered specialty carrier with significant Lloyd's presence. The London-Sydney specialty corridor has personal continuity at the most senior level, and movement between London Market carriers and Australian specialty platforms is a long-established pattern. What is new is the timing concentration: senior moves during a contested acquisition window have different competitive implications than the same moves in a stable ownership period.

Lloyd's Australian market position is similarly long-standing. The 150-year continuous presence means Lloyd's sits structurally inside Australian specialty distribution in ways that pre-date most modern competition policy frameworks. The ACCC's January 2026 merger rule changes are the first significant update to how cross-border specialty M&A gets assessed in a generation. Beazley-Zurich is the first major test under the new framework.

Why this matters for London Market acquirers

Australia's merger notification regime changed in January 2026, with the ACCC now assessing transactions earlier and with broader information powers. The Beazley review is one of the first major specialty transactions to land under the new rules. How the ACCC frames its remedies, particularly against Lloyd's-distributed business, will inform every subsequent specialty acquisition that touches the Australian market.

That is most specialty acquisitions of any meaningful size. The named transactions in the current consolidation wave, Inigo to Radian, IQUW to Starr, Beazley to Zurich, Convex to Onex and AIG, all have Australian exposure of some form. The Inigo and Convex deals completed before the new ACCC rules took effect in January 2026. Those carriers' Australian footprints, whether through service companies, coverholders, or direct syndicate exposure, did not trigger comparable competitive overlap review.

From January 2026 onwards, any specialty acquisition with Australian-distributed lines will face the same questions Zurich-Beazley is now facing. The Beazley review puts a marker down about what the next round will look like.

What to watch

Two things to watch in the next eight weeks. First, whether the ACCC's early July position frames competitive overlap as remediable against Lloyd's syndicate distribution, or escalates to a Phase 2 review with longer timelines. Phase 2 reviews typically run six months or longer and can require detailed information disclosure from the parties, which can complicate global completion timetables.

Second, whether other regulators in other jurisdictions, particularly Canada and Singapore where Beazley also operates through Lloyd's structures, raise similar questions on the same deal. Cross-jurisdictional regulatory coordination is increasing. The PRA has already approved the change of control in the UK, but parallel reviews in other markets could surface comparable structural questions.

The integration design implication

The transaction will close. Zurich has the financing and the strategic logic. The question is what shape Beazley's Australian distribution takes inside the combined entity once the regulatory process has done its work.

For London Market acquirers planning specialty deals with Australian exposure, the structural question to ask up front is no longer just whether the combined entity meets local capital and licensing requirements. It is whether the distribution model can absorb a competitive remedy if the regulator decides to apply one. That changes the integration design conversation before the deal is even announced.

The next specialty M&A target list is shaping up across Bermudian and London Market platforms. For acquirers building their integration thesis, the ACCC's framing in this case is worth tracking line by line. It defines what the next round of regulatory scrutiny will demand.

For acquirers and integration teams working through these structural questions, contact Grant.Bodie@CavehillConsulting.com or visit our consulting partners SITP at https://sitp.london/partner/cavehill.

Recent News

Our Latest Stories.